In a recent discussion, I came across a striking claim: that elite schools do not primarily sell education, but rather trust, status, and access.

It is a compelling idea—and one that resonates with many parents’ decision-making. But it also risks oversimplifying a much more important question:

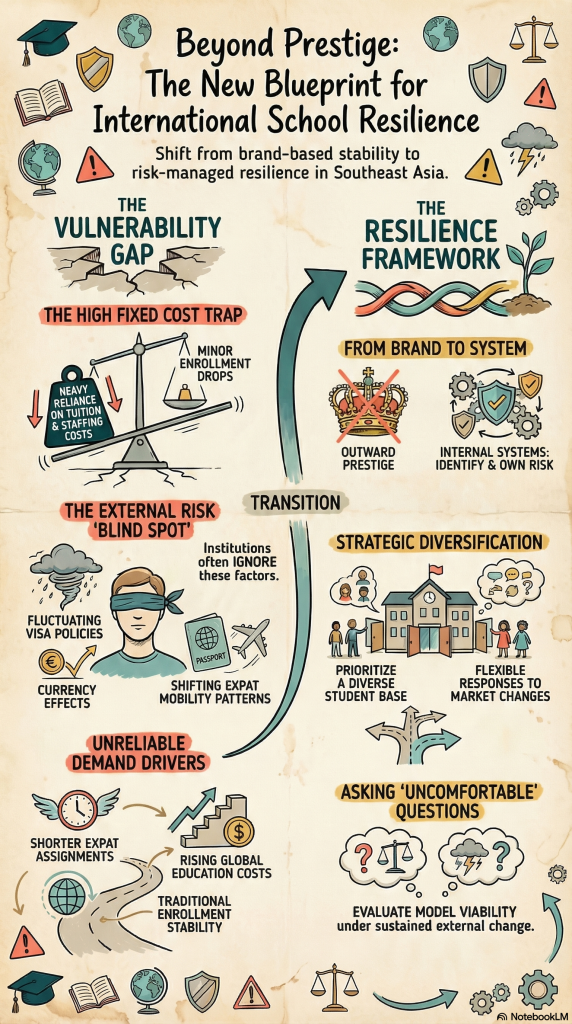

What actually makes an educational institution resilient?

Having worked across different education contexts, particularly in Southeast Asia, I find that the more interesting issue is not what drives demand in the short term, but what sustains institutions when conditions become less predictable.

A Shift That Is Easy to Miss

For a long time, international schools in Southeast Asia operated under relatively stable conditions. Demand was supported by a combination of expat inflows, growing local affluence, and a widely accepted belief in the value of international education pathways.

That environment has changed. Not abruptly, but gradually—and in ways that are easy to underestimate. Expat populations are less predictable than they used to be. Assignments are shorter, hiring is more localized, and mobility patterns have shifted since COVID. At the same time, the international university pathway—one of the central value propositions of many schools—has become less straightforward. Visa policies fluctuate, geopolitical tensions influence student mobility, and the cost of studying abroad continues to rise.

Even among affluent families, this is beginning to influence decision-making.

When Demand Becomes Less Certain

What I find particularly interesting is how these external shifts interact with the internal structure of many schools. A large number of international schools—regardless of whether they are independently run or part of larger groups—share similar characteristics:

- a high fixed cost base, driven primarily by staffing

- strong dependence on tuition revenue

- growth assumptions that are, implicitly or explicitly, built on relatively stable enrollment

Under stable conditions, this model works well. Under more volatile conditions, it becomes more sensitive than it might initially appear.

A moderate decline in enrollment does not just affect growth. It puts pressure on the very elements that underpin the school’s value proposition—its people, its programs, and ultimately its reputation.

The Blind Spot: External Risk

In many conversations about school quality, the focus is still predominantly internal: curriculum, teaching standards, leadership, facilities. All of these matter. But they do not fully capture the risk landscape schools are operating in today. What is often less developed is a systematic view of external risk, including:

- shifts in expat populations and foreign investment patterns

- changes in visa regimes and international student mobility

- increasing price sensitivity due to inflation and rising global education costs

- currency effects that indirectly increase tuition burdens

- the emergence of credible local and hybrid alternatives

Individually, these factors may seem manageable. Taken together, they create a level of uncertainty that many institutions are not yet fully structured to address.

Not All Schools Are Equally Exposed

It would be too simplistic to generalize. Some international schools—particularly those that are part of larger, well-managed groups—have more developed systems, stronger governance, and greater financial resilience. Others operate with a high degree of professionalism but remain structurally dependent on a relatively narrow demand base.

And then there is a segment where brand perception plays a significant role, sometimes exceeding the depth of the underlying system. The differences are not always visible from the outside. But they become more apparent when conditions change.

From Brand to Resilience

In stable markets, brand can carry significant weight. It signals quality, reduces perceived risk for families, and supports pricing power. In less stable environments, other factors start to matter more.

Resilience becomes a function of:

- how well a school understands its demand drivers

- how flexibly it can respond to changes in enrollment

- how diversified its student base is

- and how clearly risks are identified, owned, and managed

This is not about replacing one model with another. It is about expanding the lens.

A Different Set of Questions

Instead of focusing primarily on positioning and outcomes, it may be worth asking:

- What assumptions is this model built on—and how stable are they?

- How sensitive is the institution to changes in enrollment?

- Which risks are actively managed, and which are implicitly accepted?

- What would happen if external conditions changed for a sustained period of time?

These are not always comfortable questions. But they are increasingly relevant.

Closing Thought

International education in Southeast Asia is not losing its relevance. In many ways, it remains an attractive and growing sector. At the same time, the environment in which it operates is becoming more complex. Prestige and positioning will continue to matter. But they may no longer be sufficient on their own.

What will likely differentiate institutions over the coming years is not just how they present themselves—but how well they understand and navigate the conditions they operate in.